Big banks including JP Morgan Chase and Wells Fargo have promised to divest from fossil fuels but continue to fund unsustainable animal agriculture.

As global banking giants and investment firms vow to divest from polluting energy companies, they’re continuing to bankroll another major driver of the climate crisis: food and farming corporations that are responsible, directly or indirectly, for cutting down vast carbon-storing forests and spewing greenhouse gas emissions into the atmosphere.

“Animal protein and even dairy is likely, and already has started to become, the new oil and gas.”

These agricultural investments, largely unnoticed and unchecked, represent a potentially catastrophic blind spot. “Animal protein and even dairy is likely, and already has started to become, the new oil and gas,” said Bruno Sarda, the former North America president of CDP, a framework through which companies disclose their carbon emissions. “This is the biggest source of emissions that doesn’t have a target on its back.”

By pouring money into emissions-intensive agriculture, banks and investors are making a dangerous bet on the world’s growing demand for food, especially foods that are the greatest source of emissions in the food system: meat and dairy.

“If you look at emissions just from the largest meat and dairy companies, and the trajectories they have, you see that these companies and their models are completely unsustainable.”

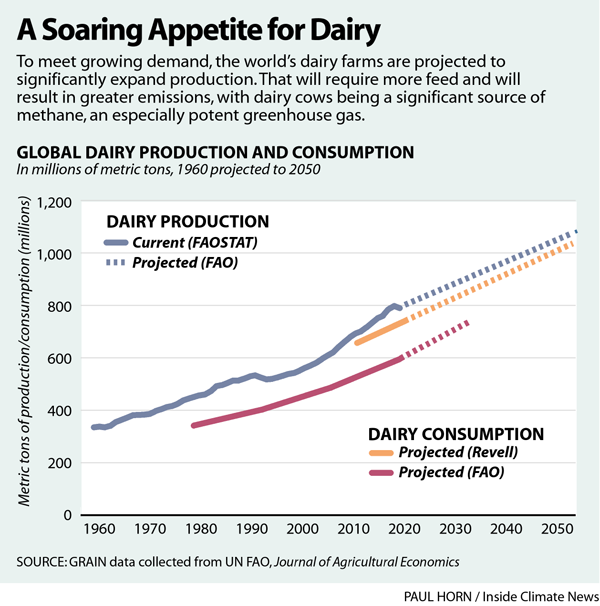

Agriculture and deforestation, largely driven by livestock production, are responsible for nearly one quarter of global greenhouse gas emissions. By 2030, livestock production alone could consume nearly half the world’s carbon budget, the amount of greenhouse gas the world can emit without blowing past global climate targets. “It’s not enough to divest from fossil fuel,” said Devlin Kuyek, a senior researcher at GRAIN, a non-profit organization that advocates for small farms. “If you look at emissions just from the largest meat and dairy companies, and the trajectories they have, you see that these companies and their models are completely unsustainable.” Those trajectories could put global climate goals well out of reach.

The American banks that are the four leading financiers, globally, of fossil fuels – JP Morgan Chase, Wells Fargo, Citigroup and Bank of America – all, to varying degrees, have made climate action more of a priority. But these and other major global banks continue to funnel dollars into companies that trade in “soft commodities,” including beef, soy, timber and palm oil, that are linked to the destruction of forests and critically important ecosystems.

A battery of recent analyses by sustainable investment and environmental advocacy groups has tracked the dollars. JP Morgan Chase, for example, has directed more than $450 million since 2016 to leading Brazilian meat packers that environmental groups claim have direct ties to deforestation and to recent devastating fires in the Amazon. BNP Paribas and HSBC are among the banks that have committed to stop funding deforestation from agriculture, but still continue to provide billions to companies that have not.

Though they have promised to address climate change, Rabobank, Morgan Stanley, Barclays and Goldman Sachs continue funding agribusinesses directly or indirectly involved in deforestation or high-carbon agriculture. The banks either declined to comment for this article or did not respond to requests for comment. HSBC and Morgan Stanley pointed to their sustainability commitments online.

“We’re still trying to get the banks to recognize that the land-use sector is part of the climate problem,” said Hana Heineken, a senior campaigner with the Rainforest Action Network, an advocacy group that has extensively tracked how banks have financed deforestation. “As things stand right now, there is still a disconnect between banks saying they’re going to address climate change in their portfolios and what they’re going to do about financing.”

The world’s largest asset managers – BlackRock, Vanguard and State Street – sell investment funds marketed as “sustainable.” But some of these funds contain agribusiness companies blamed for cutting down tropical forests. And the asset managers are among the biggest investors in major meat and dairy companies, including JBS, the world’s largest beef producer. None of these asset managers has a formal policy on deforestation, environmental groups say.

When reached for comment, the asset managers pointed to their sustainability platforms online and noted increased efforts to address deforestation and climate impacts from agriculture in their portfolios. In early 2020, BlackRock acknowledged the climate impacts of certain agribusiness practices and said it would push for greater disclosure of sustainability measures from companies in its funds.

The world’s food system needs to feed a population expected to hit 10 billion by 2050, meaning that the system will have 3 billion more people to feed than it did a decade ago. Global investors and banks see an opportunity in these numbers and, in some cases, are doubling down. The climate impact of this could be disastrous, with emissions from the food system projected to rise by nearly 60 percent if they stay on their current path.

Faced with these dire numbers, some critics are increasingly calling for divestment from the food and agriculture companies with the biggest climate impacts – especially giant livestock and grain companies – much as they’ve called for divestment from fossil fuel companies. Others are simply calling for more vigilance in policing destructive farming practices and the financial institutions that support them. They’re also pushing for more support for farmers and farming methods that use fewer resources, emit fewer greenhouse gases and replenish soils. “We need food,” said Moira Birss, climate and finance director for Amazon Watch. “And we don’t need fossil fuels.”

As demand for food rises, the world’s banks and investors will ultimately determine whether an increasingly taxed food system fuels a climate collapse.

Big banks have big impacts

Agriculture is the biggest driver of deforestation globally, responsible for half of all recent tree loss and more than 90 percent in the tropics.

Palm oil, soy and cattle are the largest commodities behind that loss, with cattle accounting for from half to two-thirds, as agribusiness interests or their suppliers cut down or burn forests to open up more pasture to graze the animals or cropland to feed them. These commodities, known as “soft commodities” because they are grown, not extracted, pose the most significant risks to forests. They are also the keys to profit for the agriculture and food industries.

Clearing forests releases huge amounts of carbon dioxide and destroys their ability to store carbon. It’s also a major cause of soil erosion and biodiversity loss, which create yet more risk to the global food supply and to public health, as the coronavirus pandemic has so clearly illustrated. With the destruction of large ecosystems, biodiversity plummets. The species that survive tend to be the ones that harbor and spread disease.

While the burning of fossil fuels remains the largest contributor to greenhouse gas emissions, emissions from agriculture would have to be slashed to stay within the 1.5 to 2 degrees Celsius targets of the Paris climate agreement. That’s even if the rest of the economy, including the energy and transportation sectors, adequately decarbonized.

Stopping deforestation is one of the fastest ways to limit carbon emissions. Yet the world’s biggest banks and asset managers are fueling the problem instead. The UK-based group Global Canopy examined the companies with the greatest exposure to deforestation, including financial institutions. It found that, despite making commitments to stop deforestation by 2020, as of 2018, not a single company was on track to cut deforestation from its supply chains. These included a range of companies that rely on commodities tied to deforestation, including McDonald’s and PepsiCo.

Banks, Global Canopy concluded, were the biggest laggards: “Financial institutions are behind companies in setting commitments and policies on deforestation. Of the 150 financial institutions assessed, nearly two-thirds had no financing policy for any of the four key forest-risk commodities,” their report said. In its 2020 analysis, the group found 63 percent of financial institutions still did not have deforestation policies. This despite the banks’ outward claims and commitments to tackling climate change.

In fact, the world’s major banks are accelerating their funding of commodities tied to deforestation in Latin America, Africa and Southeast Asia. Among the top banks funding “forest-risk” commodities – those potentially responsible for deforestation – are JP Morgan Chase and Rabobank, the world’s leading agricultural bank, which has said it does not fund deforestation in any areas of Brazil.

Many of their commitments – public and much applauded – have come since the Paris climate agreement. Yet, as with the funding of fossil fuels, the money they are investing has ballooned since the historic accord. Overall, global banks have increased their lending to commodities linked to deforestation by about 40 percent, funnelling $154 billion in credit from December 2015, when the agreement was signed, to April of last year. Most of these forests are being converted into cropland, to grow grain to feed livestock, or to pastureland, to graze cattle. The conversion doesn’t just destroy forests, releasing carbon dioxide in the process, it multiplies the number of animals that emit methane, an especially potent greenhouse gas.

Financial think tanks and green investment groups, in report after report, have found that major global banks have made promises to stop financing deforestation, but have not lived up to them.

Not a single major bank that has committed to stop financing deforestation from soft commodities has done so completely or quickly enough, according to a December report from BankTrack. And no American bank has required its clients to adopt no-deforestation policies.

JP Morgan, Citigroup and Bank of America are among the top US-based creditors of American commodities giants Cargill, Bunge and ADM, which supply major American food businesses, from McDonald’s to Walmart. These grain traders have made commitments to stop deforestation, but continue to come under fire for their vast soy plantations, one of the largest drivers of deforestation in South America. Cargill and Bunge did not respond to requests for comment.

Edel Bach, a spokesman for JBS, said the company has a “zero-tolerance approach to illegal deforestation” and “has made extensive investments… to monitor its entire Amazon value chain to ensure it is illegal deforestation free by 2025.”

Jackie Anderson, a spokeswoman for ADM, explained that the company has a no-deforestation policy, is a signatory to a moratorium on deforestation in the Amazon and is a founding member of the Soft Commodities Forum, an effort to stop deforestation and land conversion in the soy supply chain.

Recent research has found that, despite making these commitments, the major grain traders are still producing commodities that are tied to deforestation in areas of Brazil beyond the Amazon. These same companies continue to be blamed for deforestation linked to palm oil in Southeast Asia, much of which ends up in products made by top international consumer goods companies.

The role of the Asset Managers

The biggest asset managers, led by BlackRock, are also significantly invested in the meat and dairy industries and in other commodities linked with deforestation.

Though meat and dairy account for less than 1 percent of their total assets under management, BlackRock, Capital Group and Vanguard are the meat and dairy industries’ largest shareholders, according to Feedback Global. Blackrock and Vanguard are also JP Morgan’s largest shareholders.

BlackRock, Vanguard and State Street – “The Big Three” asset managers – have $12 billion invested in producers linked to deforestation, including the major grain traders ADM, Bunge and Cargill, and the meatpackers JBS, Marfrig and Minerva, according to a recent analysis by Friends of the Earth. ADM, Bunge, Cargill and JBS, in turn, indirectly and directly supply some of the world’s biggest consumer goods companies, including PepsiCo, Nestlé and Unilever.

The report puts much of the blame on the big asset managers. “Powerful investors have consistently undermined meaningful action by agribusinesses and the consumer goods sector writ large,” the analysis said.

The asset managers say they have no control over the companies in their funds, because the majority of their investment products are passively managed index funds. These types of funds follow a major market index, like the S&P 500, which means the index manager actually controls which companies are in the fund. “Every dollar that BlackRock manages belongs to our clients, and more than 90{85424e366b324f7465dc80d56c21055464082cc00b76c51558805a981c8fcd63} of our equity assets are invested in index-based funds that our clients choose,” a spokesman for BlackRock responded in an email. “We cannot selectively divest from individual companies in indexes that may present sustainability risks.”

A Vanguard spokesperson said that while there is “no industry acknowledged specific exclusion regarding deforestation,” Vanguard’s sustainability funds track an index that filters out companies that fail to align with principles outlined by the United Nations. (These do not explicitly mention deforestation.)

State Street and Capital Advisors pointed to their sustainability statements online. But critics say that the Big Three and other major asset managers are getting a pass, and that they could exclude certain companies from their basket of investments if they implemented no-deforestation policies or structured their products differently.

“They could put in place explicit screening tools,” said Matthew McLuckie, managing partner at Posaidon Capital, a London and Zurich-based green investment firm. “If you are going to support a net-zero transition or Paris alignment, how can you be holding companies chopping down tropical forests?”

In emailed responses to questions about their deforestation practices, McDonald’s, Nestlé, Unilever and Walmart said that they had made commitments to source their products only from deforestation-free areas: McDonald’s said it would eliminate deforestation from its supply chain by 2030; Nestlé said it would stop sourcing soy and palm from deforested areas by 2022 and stopped buying Brazilian soybeans from Cargill in 2019; Unilever said its supply chains would be deforestation-free by 2023; Walmart said it would stop sourcing beef in deforested areas of Brazil by 2022, among other commitments. PepsiCo did not respond to a request for comment.

Disclosure is voluntary

Over the last decade, investors and regulators have pushed companies, including financial institutions, to disclose their carbon emissions. Disclosure is a key first step toward giving investors and banks the information they need to make informed decisions about where to put – or not to put – their money.

Guidelines, like those outlined by the Taskforce on Climate-related Financial Disclosures (TCFD), and platforms, including the CDP (formerly the Climate Disclosure Project), have prompted greater responses from a growing number of companies that see climate change as a risk.

Without disclosures, banks and investors aren’t equipped with information about the greenhouse gas impacts of the companies, including banks, that they invest in or support. But these disclosure requirements are voluntary and, critically, they don’t comprehensively reveal the extent of deforestation or other climate risks in companies’ agricultural supply chains.

The TFCD guidelines, the most robust and widely used, explicitly say that banks don’t have to disclose emissions from agriculture. Rather, the task force “suggests banks define carbon-related assets as those assets tied to the energy and utilities sectors.” That means for banks, at least in the framework of the TCFD, agriculture isn’t a “carbon-related” asset, so banks don’t have to reveal the extent to which they finance them.

Critics say this allows banks and the companies they finance to hide behind their supply chains. JP Morgan’s first report using the TCFD guidelines, for example, contains no mention of the bank’s investment in commodities with ties to deforestation.

Most of the emissions from agriculture and food companies come from their “Scope 3” emissions – emissions not from their direct operations, but from their supply chains. Nearly 90 percent of food and agribusiness company emissions fall into this category, experts say, but only a fraction of the companies report them. Of the world’s top food and beverage companies, only 16 percent disclose emissions from their agricultural supply chains.

Many companies don’t report on the deforestation in their supply chains at all. Those include Domino’s Pizza and Mondelez. And even those that do disclose may not, depending on the company, include a complete picture of emissions from deforestation or, importantly, the conversion of land from forest to pasture or cropland. A Domino’s spokesman said the company provides information on sourcing for its U.S. products on its website and is currently developing a climate strategy. Mondelez did not reply to a request for comment.

Part of the problem is not just the general murkiness of supply chains, but a lack of common principles for measuring emissions from land conversion and deforestation. “In greenhouse gas accounting of Scope 3 emissions, it’s challenging to get high quality data because they don’t have a lot of transparency in their supply chains,” said Cynthia Cummis, a greenhouse gas accounting expert with the World Resources Institute. “The science behind land-based emissions is challenging and there isn’t agreement on the best methods.”

Companies can take advantage of that, critics say. The data self-reported to CDP by the companies is not audited by a third party, and critics say CDP’s rating system rewards companies for having a policy on deforestation, even if that policy is weak. “In effect, you’re taking a company’s word,” said McLuckie. “Investors are left largely in the dark.”

‘This is just about money’

Demand for “green” investments that meet environmental standards has grown in recent years, as progressive investors pressure companies to address climate change. “Impact investing” has gained traction with investors, and sustainable funds now control more than $1 trillion in assets, doubling, according to a 2020 analysis by Morningstar, over the three years before the study.

A 2019 report from the Croatan Institute found that impact investing now accounts for more than $17 trillion – or one in three dollars – of the more than $51 trillion in assets under professional management, a 42 percent increase over 2018.

In a January 2020 commentary, BlackRock acknowledged that agribusinesses have a significant climate impact, especially because of their links to deforestation, and said that the company would engage with those companies to improve their performance. “Amongst other things, we ask companies to disclose any initiatives and externally developed codes of conduct, e.g. committing to deforestation-free supply chains, to which they adhere and to report on outcomes, ideally with some level of independent review,” the company reported.

But some of BlackRock’s sustainable investment funds contain large agribusiness companies with ties to deforestation. For a company to be included in the fund, it needs to provide an inventory of its greenhouse gas emissions, but not its Scope 3 emissions. “You have huge agroindustrial companies —chemical, fertilizer, seed monopolies— in these so-called sustainability funds,” said Mark Campanale, executive director of Carbon Tracker. “If they’re the answer, we’re asking the wrong questions.”

Giant fund managers establish criteria for the risk they’ll take on in their portfolios, but, because of the lack of transparency and uniform standards on disclosure, they may not know the extent of the emissions from any given company. Companies with supply chains linked to deforestation often defend themselves by saying that the supply chains are too complicated to monitor effectively, and that doing so would be prohibitively expensive.

Some companies, notably Unilever, are investing millions to clarify their supply chains so investors and consumers know exactly where their products are sourced. But many companies hide behind their supply chains, some analysts say. “They try to do everything they can to be intransparent in their supply chains,” said Gerard Rijk, senior equity analyst with Profundo, a Netherlands-based research group that tracks supply chains and investing. “It’s clear they’re not trying hard enough. This is just about money.”

One initiative, the Partnership for Carbon Accounting Financials (PCAF), created a system that enables financial institutions to assess their “financed emissions.” Like supply chain emissions, a financial institution’s loans and investments are Scope 3 emissions, and represent the vast majority of their emissions. In July, Morgan Stanley became the first U.S. banking giant to join PCAF. It was followed soon after by Bank of America and Citi. As of February 2021, PCAF included 101 financial institutions, representing more than $21 trillion in assets. But PCAF’s methodology, a work in progress, does not yet encompass carbon emitted from land-use conversion, when land is changed from forest to crop or pastureland, one of the biggest sources of emissions from agriculture.

Doubling down

To feed 10 billion people by 2050, the world needs to produce 50 to 70 percent more food. For investors, those are appealing figures. “Demand is going up and there’s a lot of money to be made,” said Merel van der Mark, coordinator of the forests and finance coalition for the Rainforest Action Network.

In a 2018 report, Valoral Advisors said there were roughly 440 funds in the food and agriculture sector, up from 38 in 2005. Those funds managed around $73 billion in investments. “The last 10 years have seen the emergence of the global F&A sector as an institutional asset class with increasing interest from private and institutional investors alike,” Valoral said, referring to the food and agriculture sector.

Indeed, investors seem to be doubling down, in part because they’re getting a strong message about future demand. That’s true for food of all kinds, but especially for meat and dairy, as appetites and incomes rise in developing countries.

A marked uptick in agricultural investing occurred after the 2008 financial crisis, when global food prices spiked and investors began seeing opportunities, especially in farmland. “Within the financial sector there’s just been an evolving and growing effort to find returns wherever they can, and it’s moving beyond your traditional investments,” said Kuyek, of GRAIN. “That’s part of the reason you’re seeing investment in agriculture.”

The profits to be made from meat and dairy are especially enticing, largely because of rising demand, but also because low grain prices have made it increasingly cheap to produce beef and milk at lower costs. “There’s been a meat-ification of diets, particularly in the US, Europe, Brazil and Australia, and increasingly, China,” said Daniel Jones, a senior campaign manager with Feedback. “We know that meat and dairy is a climate issue, but why is it that meat and dairy continue to grow? Is it an insatiable human appetite for meat? Probably not.”

Saying but not doing

As investors increasingly move toward investing in sustainable investment funds and impact investing grows, shareholders and green-focused asset managers have been pushing companies to tackle their climate impacts. They do this through a range of actions, including putting forward shareholder resolutions requesting climate action.

Because the giant asset managers are often the largest shareholders in corporations – including banks – their votes can determine whether a resolution passes or not. And, for the most part, even asset managers that have committed to addressing climate change often have failed to support climate-related resolutions. In 2020, for example, BlackRock and Vanguard voted against climate-related resolutions more than 80 percent of the time. On agriculture-specific resolutions, the numbers are even lower.

In cases where BlackRock did vote with shareholder proposals in favor of climate action, the companies it targeted were largely energy companies, not those with agricultural supply chains and links to deforestation. Since 2012, the Big Three have voted against, or abstained from, 16 shareholder proposals aimed specifically at deforestation. (In a notable exception, BlackRock voted in 2020 to support a shareholder proposal at Procter & Gamble that asked the company to report on its efforts to eliminate deforestation in its supply chain).

“There’s absolutely a big gap, full-stop,” said Jessye Waxman, shareholder advocate with Green Century Funds. “I think this speaks to the broader questions about what it really means for a firm to be addressing climate risk comprehensively. If you want to address climate risk, you need to address agriculture.”

Feedback Global and other critics contend that engagement – from appealing to companies directly to shareholder resolutions – isn’t working. They’re now calling for divestment from carbon-intensive agricultural and livestock companies.

Still other critics say that banks and investors have an opportunity to influence companies toward more sustainable forms of agriculture. “Our call isn’t for full and immediate divestment from the agriculture industry as it essentially is for fossil fuels,” said Birss, of Amazon Watch. “It’s not the same. We can’t say it’s all terrible.”

But, she added, “If irreparable harms to the climate come from the production of food, those who are carrying out the production of that food and the people providing the one necessary ingredient – finance – have a responsibility to ensure those irreparable harms aren’t happening.”

Original source: https://insideclimatenews.org